Table of contents

- What is a payment service provider?

- What advantages do I have through a payment service provider?

- PSP or Collecting PSP - Which provider is right for me?

- Conclusion: With these payment service providers you ensure secure Payments

When you buy something in the store, you usually have two payment methods to choose from: cash or card. Especially with cash payment, it is obvious - and literally in it - who pays whom something how to settle a bill. However, things look a bit different on the internet. After all, retailers and buyers do not have to come into real contact with each other at the same time. To provide technical support specifically for online shops, some so-called payment service providers have been able to establish themselves on the market in recent years.

To understand what advantages these bring, a thought experiment: To make a cash payment successful, you need the following: cash, a wallet, a cash register system and two people who exchange money. These resources can now be transferred one-to-one to an online payment. Payment providers can cover several of these items. Because while some are only responsible for the imaginary cash register system, there are some that also include payment processing or even the wallet virtually.

The metaphor will help you understand the complex topic of payment management at the appropriate places. In this article, you will learn how to find the best payment service provider for your online business and then successfully integrate it into your payment system.

What is a payment service provider?

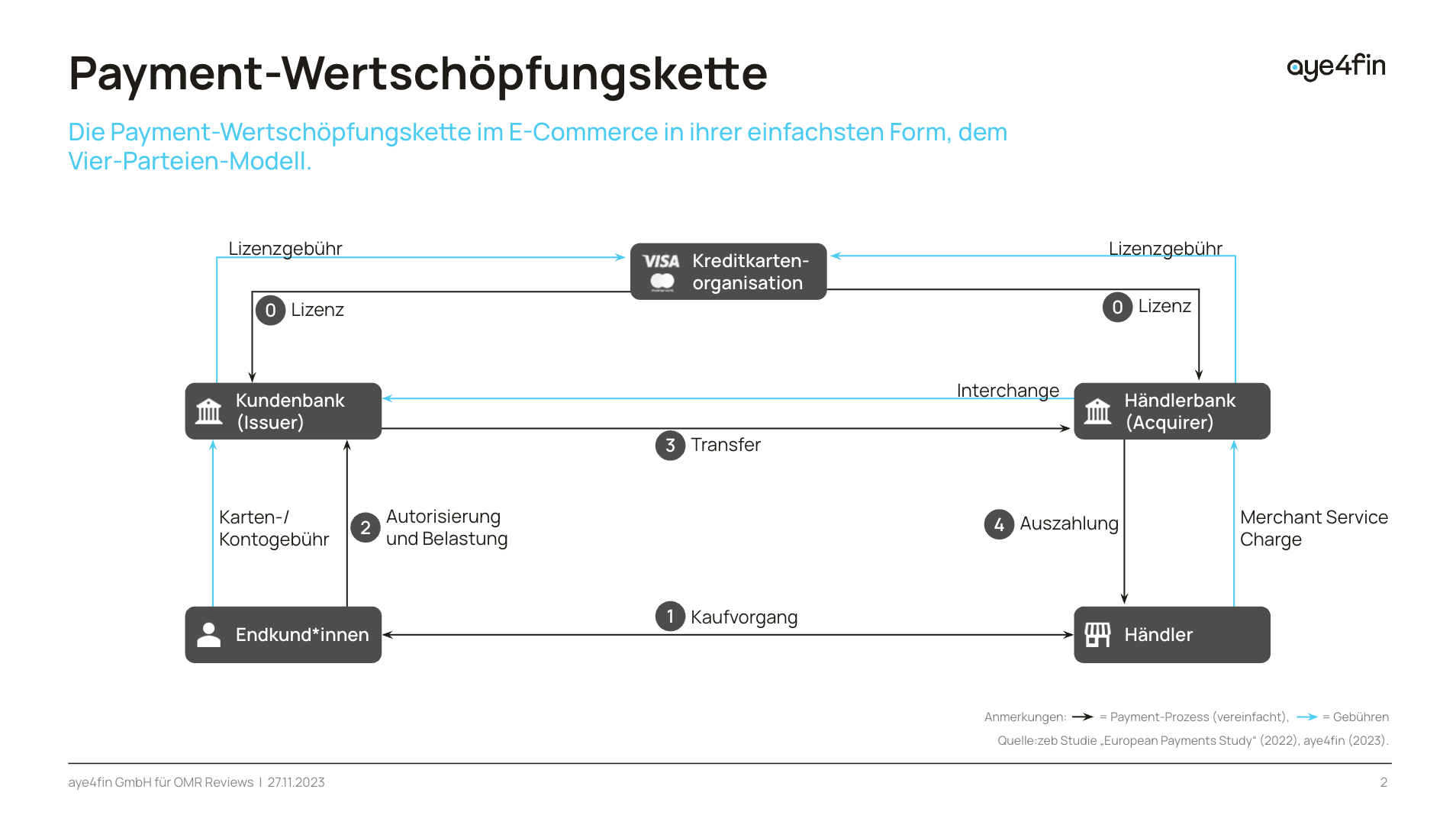

Before we start looking for the best payment tool for your online payments, let's talk a few words about the technical implementation. Since a digital payment process is quite complex, there are a few steps you should take a closer look at.

- Payment Gateway: Technical interface that enables a payment

- Processor (Processor): Processing of the payment, which sends the necessary data to all parties

- Banks (Acquirer): Start and end of the transaction

- Payment Distributor: System, which forwards payment data collected to Acquirer

With every payment on the internet, there must be a Gateway and/or a Processor for the process to be successful. In addition, banks as Acquirers must always be involved. Imagine how your customers choose their preferred payment method and a new window opens. This is the payment gateway. The processor - or the acquirer directly - then takes care of the processing after all relevant data has been entered.

In our scenario from the beginning, the payment gateway represents the cash register; the processor is the person who puts the money from the wallet into the cash register. In this way, a payment can also be carried out as self-service. Only a payment system and an executive force are needed. And of course, banks are involved in providing the money - through a previous withdrawal and a later deposit into the business account.

If you are technically fit enough and know a lot about payment systems, payment providers like ACI Worldwide or IXOPAY help you implement a gateway. If you are looking for banks that appear as acquirers in online payments, for example, it is worth taking a look at TeleCash, Barclaycard or Concardis.

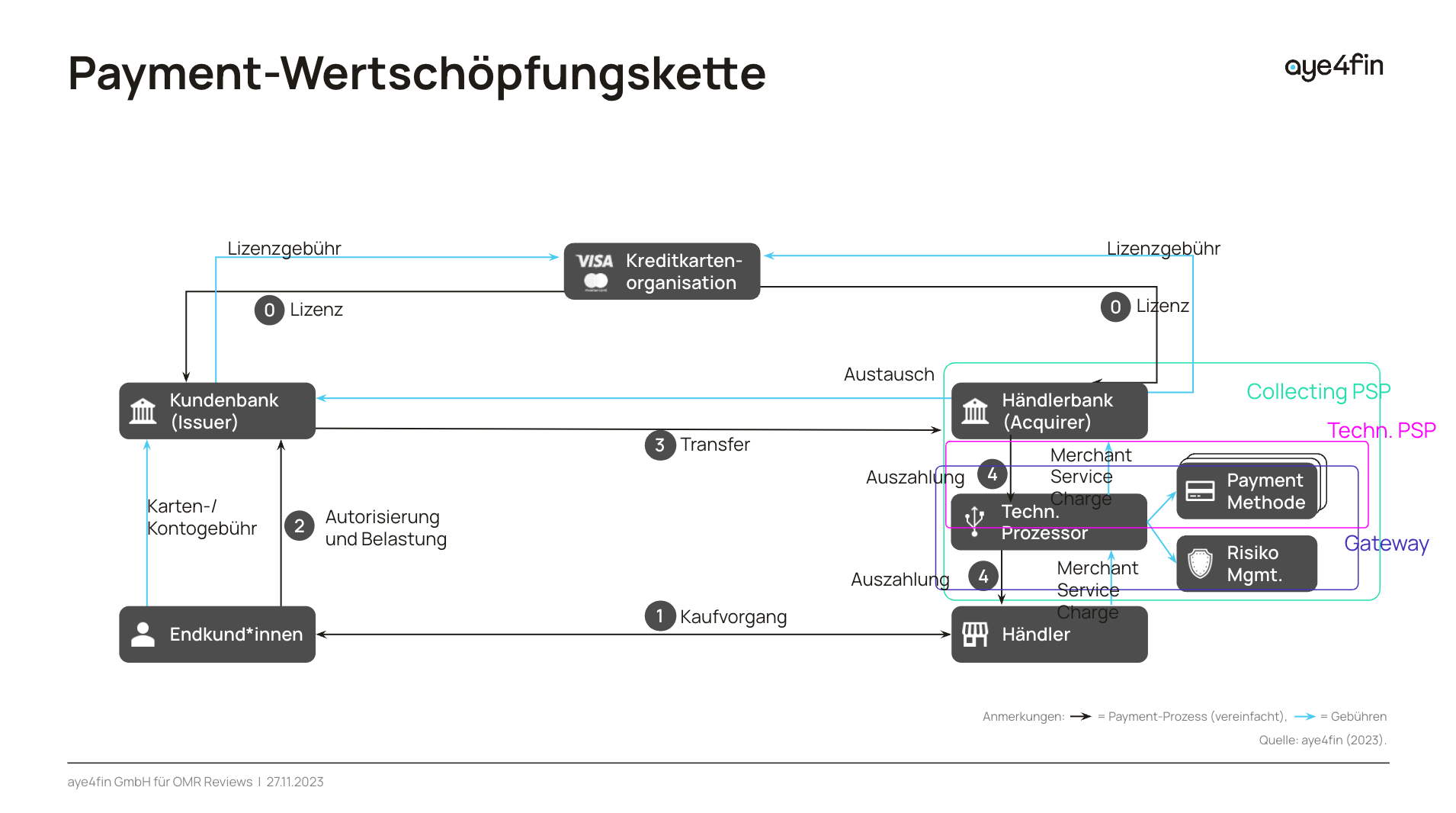

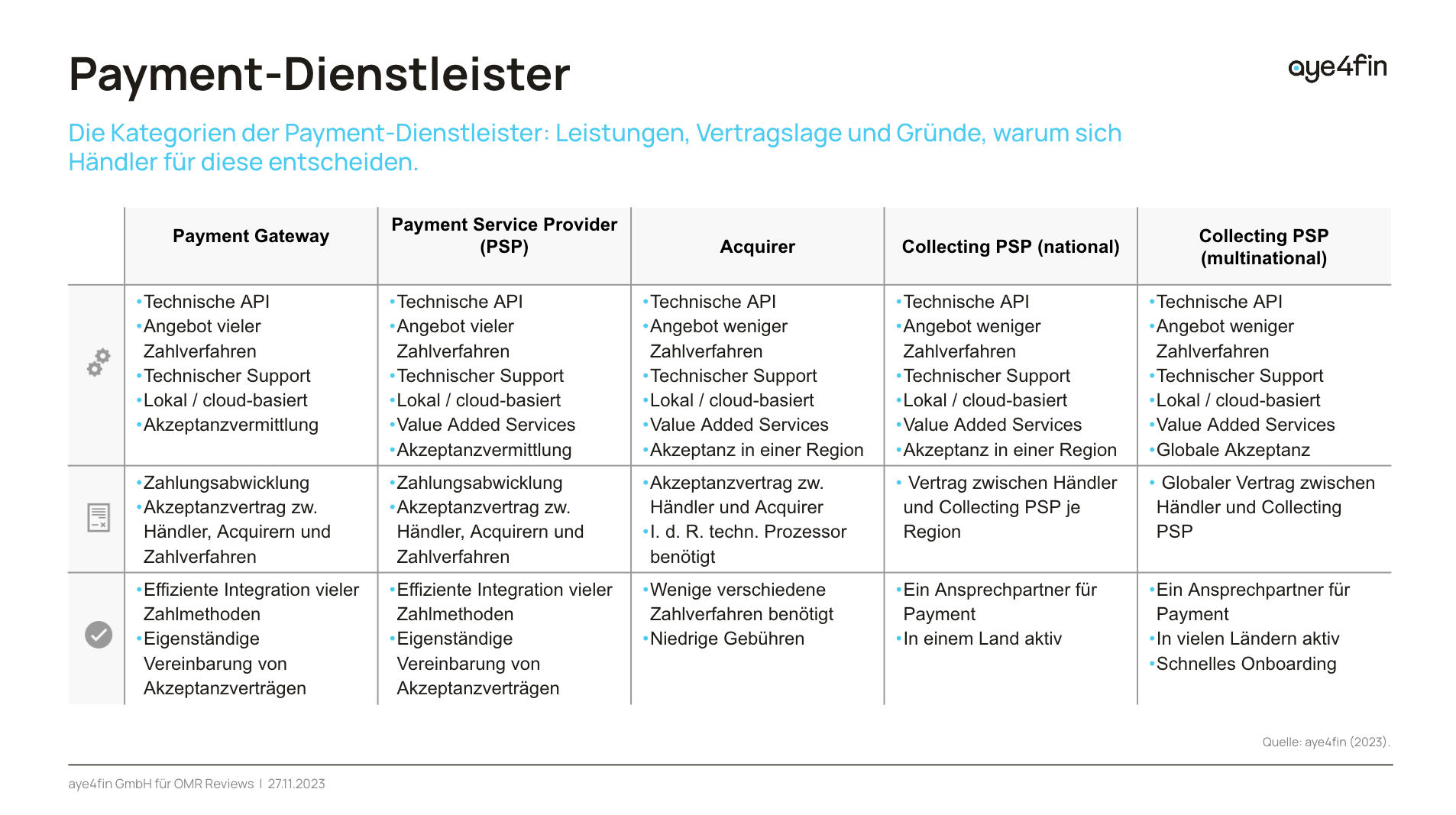

If your online shop is supposed to offer only one payment option and you can technically add the gateway yourself, you don't have to worry about a possible payment distributor. But if you need a payment distributor, you can choose between the direct acquirers or a Payment Service Provider (PSP), i.e. an external provider. There are three types of this category:

Payment Service Provider (PSP)

- Technical PSP

- Collecting PSP

- Aggregators

While Technical PSPs only regulate the digital component of payment processing, Collecting PSPs also include the entire financial administration. Thus, a technical payment provider is very close to a traditional processor and can even cover this. So-called aggregators cooperate even more closely with banks (if they are not already ones themselves). They negotiate individual conditions with the financial institutions for their customers.

For our metaphor of cash payment, this means that the payment process is carried out by another party, in our case an external cashier. The buyer no longer puts the money in the cash register himself, but third parties intervened. And now to the difference between the various PSPs: a technical provider only carries out the action, a Collecting PSP takes care of the financial component, for example discounts or gratuities. Aggregators or Acquirers are cashiers in our comparison who cooperate with the banks or come directly from them.

For the sake of completeness, it is still important to mention what payment service providers are not. Payment methods are often thrown into a pot with PSP - after all, there are tools for both that overlap in part. Here are two examples:

- A customer buys in a webshop with the payment method credit card. The Visa card is now a means of payment, she enters her data into the gateway. However, Visa or the online shop is not behind the technical integration, but a PSP, which triggers the payment from the customer's bank to the merchant's bank.

- Another customer buys a trip on the internet. He chooses the payment method transfer (Klarna Sofort). The gateway opens and the customer enters the data of his bank. Payment service provider in this case is Klarna, combined with its own Klarna Bank as Acquirer.

To what extent a PSP also represents an Acquirer depends on the bank licenses. In Germany, there are traditionally three types: Payment Institutions, E-Money Institutions and CRR Credit Institutions. Basically, different financial institutions and fintech companies differ in how large their powers are and which products they can offer customers.

PayPal for example, has a full banking license and is therefore also allowed to grant loans and manage several payment methods. In our thought game, the wallet represents the payment method. Thus, the wallet can come from one hand like the cash register system.

In addition, there are similar integration options for software for receivables, payment or accounting management. However, these are almost always not their own payment providers, but only integrate them.

elopage for example, is a Spend Management System, which has a direct connection to the PSP Stripe. And

CopeCart for example, is an online sales platform with receivables management.

What advantages do I have through a payment service provider?

The three types of payment distributors all have advantages and disadvantages. The decisive factor for your choice of a payment tool is how much control you want to give up over the transactions. Or differently: how much help you need with the processing of the payments.

Generally, you have to know that with an increasing number of payment options, the technical implementation always gets more complicated. Because for every provider of payment methods you have to set up an individual billing, if you take everything into your own hands. A payment service provider on the other hand regulates the connections for online payment traffic and builds the bridge between the merchant shop and the customers. Surely you know payment steps like the verification of your data, an encryption or the checking of the account coverage. While you as a customer can only see the gateway, the PSP takes care of everything in the background of your payment.

First and foremost, there are two convincing arguments why you should be interested in a payment service provider:

- Since an integrated tool takes over the technical implementation of the payment processing, you do not need any expertise about Payment Systems as well as their digital implementation in your user interface.

- Where you normally assume full risk with the payments, a Payment Service Provider intervenes if there is a problem with the payment. For refunds or difficulties with the banks, the PSP is responsible, not your team.

So we can conclude: To simply offer as many payment methods as possible in your online shop, no Payment Provider is necessary. This maintains the technical integration including Gateway, Processor and interaction with the banks. Similar to how you need a person at the cash register to accept cash payments.

PSP or Collecting PSP - Which provider is right for me?

The exact demarcation between the types of payment tools is not really easy. After all, many Payment Service Providers offer individual functions, so you can always decide how to implement an integration or have it implemented. If you decide for a payment service provider, you are well advised with a classic PSP or a Collecting PSP. Tend to the latter if you need more active support (risk management, fraud protection or currency conversion). You should also pay attention to whether a payment service provider can operate nationally or internationally.

Here is an overview of your payment integration options:

PSP

Collecting PSP

For more information on functionalities, feel free to take a look at

our software guide on the topic of Payments. Here you can find the most popular payment methods and payment service providers in comparison. With the large selection and complexity of the topic, you should definitely think about which PSP is the best for your online shop.

Conclusion: With these payment service providers you ensure secure Payments

To ensure that the online purchases of your customers really bring the desired sales, you can't get around a payment integration. You only increase customer satisfaction when the payment can be made digitally and as varied as possible. In this way you respond to the individual needs of your clientele. But with many payment methods, technical complexity and financial bureaucracy also increase.

Here, payment service providers offer a range of support: whether it's the technical interface (the Gateway), with or without payment processing, or the entire interaction with the banks. In most cases, classic providers for payment systems and Collecting PSP take care of all annoying or difficult matters behind the payment traffic. So you don't have to struggle with the individual invoices of the payment methods and the banks, but can take care of other to-dos of your business.

It remains complicated with the topic

Payments. Where it is still easy in stationary commerce - customers pay cash, merchants post sales -, various payment options on the internet do not make it particularly easy to keep track of interface, processing and transactions. Although there is also self-service in retail with only the purchasing person and the cash register system. However, it is much easier for everyone involved if cashiers ... i.e. payment service providers take care of the processing.

Bridgerpay

Bridgerpay checkout.com

checkout.com Mollie

Mollie Payrexx

Payrexx PAYONE

PAYONE Adyen

Adyen Klarna

Klarna Computop (Nexi) Checkout

Computop (Nexi) Checkout Stripe Payments

Stripe Payments Unzer

Unzer